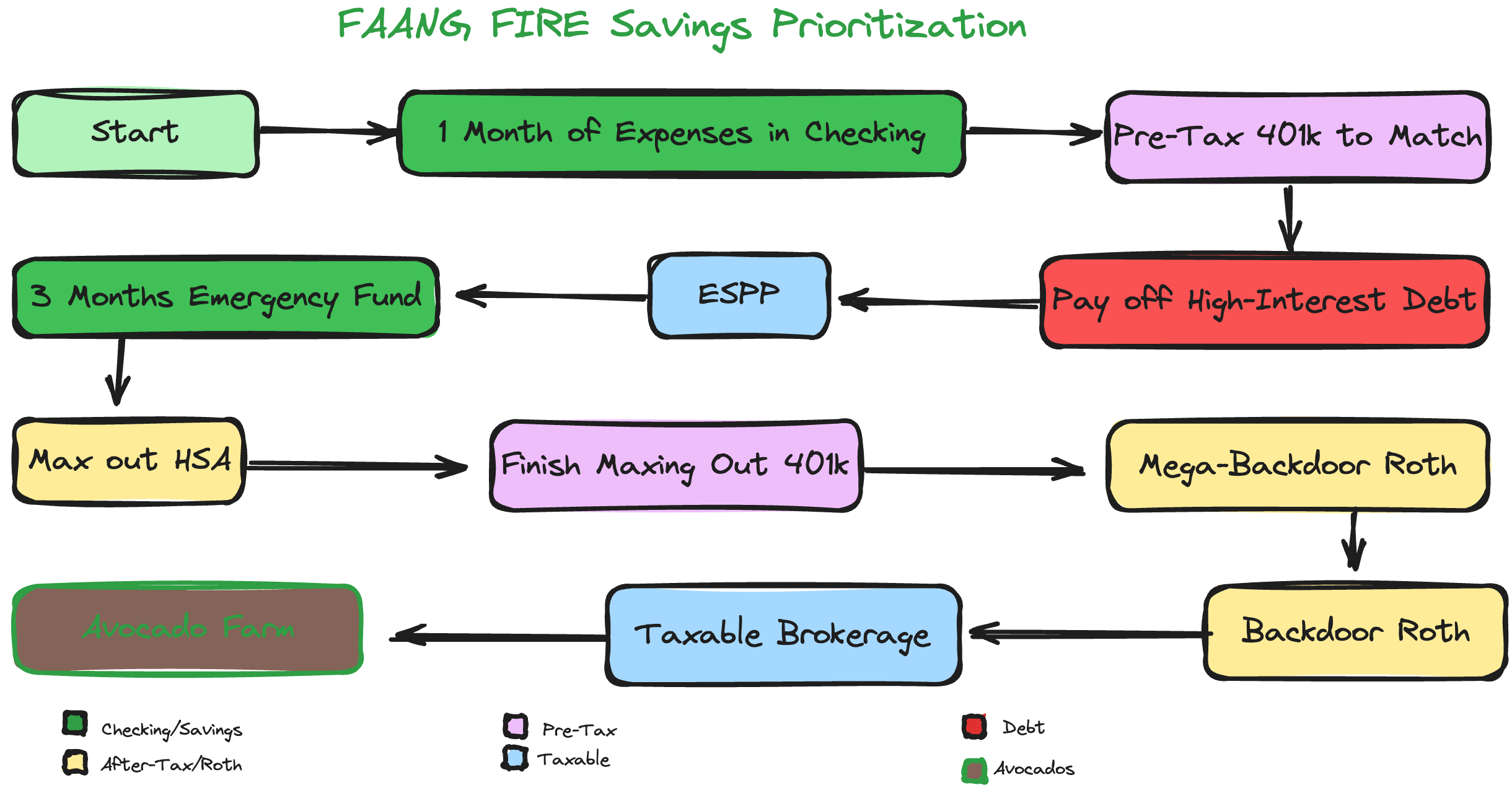

The Cash Flow Waterfall

A Breakdown of the FAANG FIRE Savings Prioritization Waterfall

I first introduced the FAANG FIRE Savings Prioritization Waterfall in the “Where I Would Save $100k Per Year” post, but I never broke down WHY things are in this order.

Let’s go through the flow chart and talk about each item to break it down. I want you to know what to do and the reasoning behind it. The reasoning is even more important because personal finance is personal, so your personal waterfall might look different than mine.

The OG FAANG FIRE Waterfall

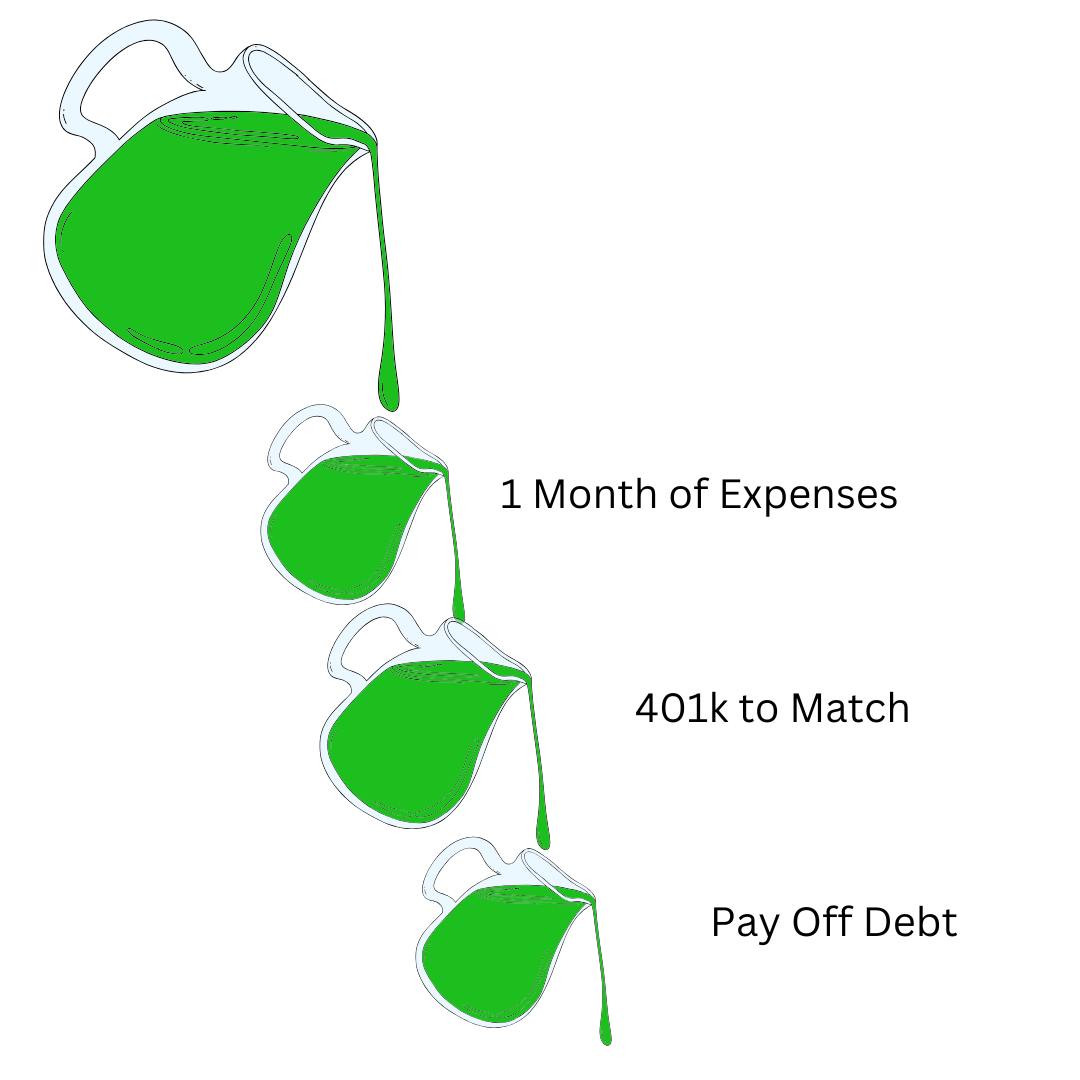

You can think of this as a bucket that fills up one section and once that section is full moves on to the next. All new money you have flows through this waterfall, regardless of whether it comes from your base salary, bonus, RSU vests, or anywhere else.

The High Level Concepts:

build an initial savings buffer to cover monthly expenses

get the 100% free money

knock out high interest debt

pick up other freeish money (espp, assuming a discount and ability to sell right away)

build a bigger cash buffer for your emergency fund (3 + months)

max out tax advantaged accounts prioritizing those that result in a tax savings today, then tax advantaged accounts that result in lifetime tax savings

build up the old reliable brokerage account.

Some of these buckets also have limits or may not apply to you. If that is the case, just skip over it!

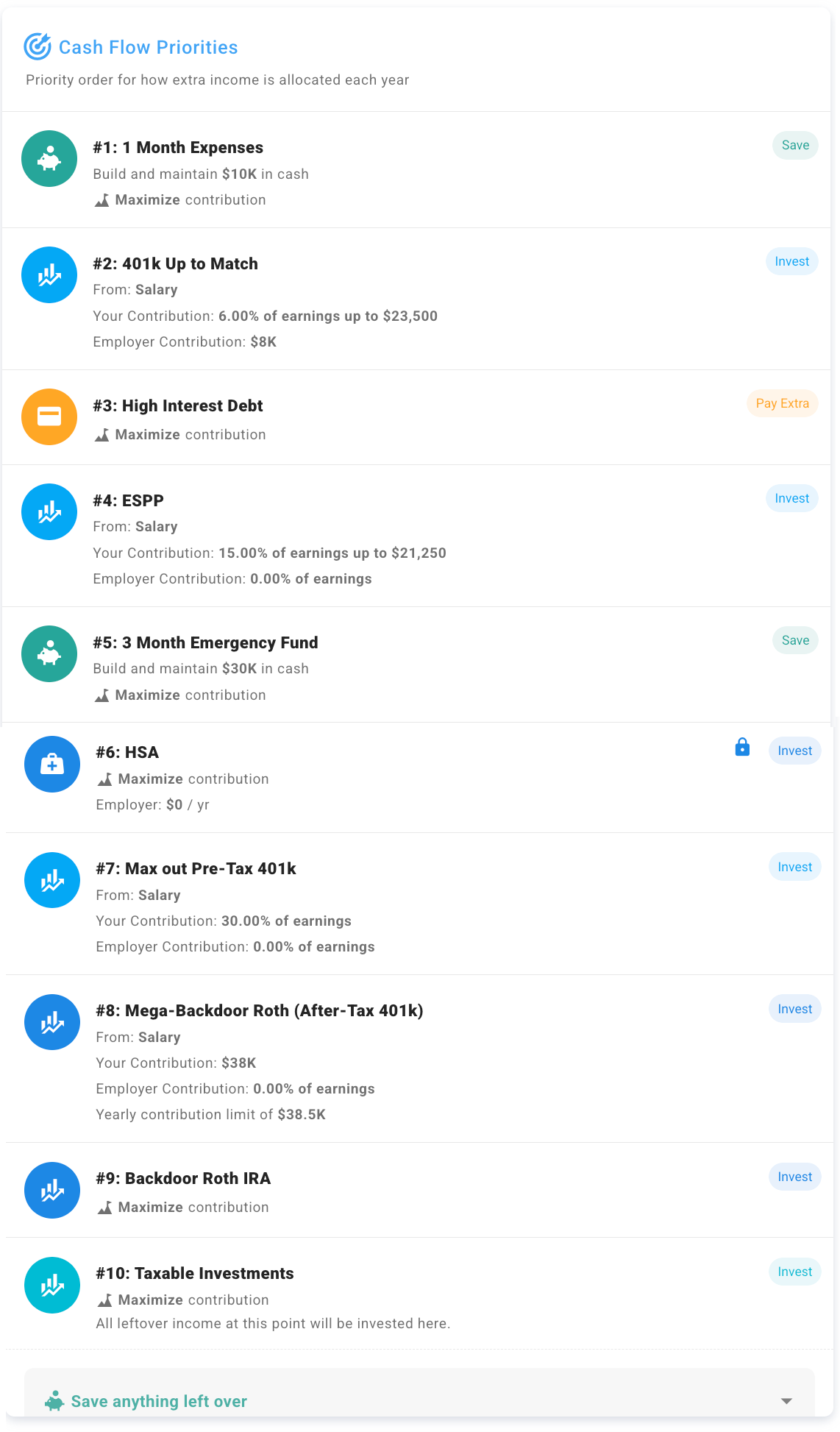

1-Month of Expenses in Checking

If you are starting your FIRE journey from scratch, it is important to set yourself up for long term success. 1-Month of expenses isn’t enough of a real buffer long term. However, if you are working at a stable W2, it is enough of an initial buffer to allow you to start prioritizing the buckets that I categorize as “free money”.

Pre-Tax 401k up to the Match

This is the first of the “free money” sections. I could spend a longer post about the nuances between Pre-Tax vs Roth here…

If you will be working for the entire year in big-tech, there is a high likelihood that the benefits of saving on taxes today by reducing your taxable income via pre-tax 401k contributions is beneficial.

This bucket will fill up once you hit the 401k match limit.

High Interest Debt Paydown

High-interest debt, such as credit card balances or personal loans with rates above 5-7%, will significantly slow your progress towards financial independence. Prioritize aggressively paying down this type of debt to save money on interest and accelerate your savings.

ESPP

An Employee Stock Purchase Plan (ESPP) typically offers shares of your company's stock at a discount, often around 15%. If your plan allows immediate sales, it's usually best to contribute to the maximum allowed, buy at a discount, then sell immediately to lock in gains without significant risk. It is limited to a pre-discount $25,000 per year contribution. This is a form of "freeish money." Just remember, the discount will be taxed.

If your plan doesn’t have a discount or has restrictions on when you can sell it can be skipped.

3-Month Emergency Fund

After securing your initial 1-month buffer, the next priority is to grow this into a more substantial emergency fund of three months of expenses. This amount provides greater peace of mind and security, protecting you from unexpected life events like job loss or unforeseen large expenses. While three months is a good starting point, you might adjust this based on your job stability, comfort level, and personal circumstances.

If you are more conservative, are the sole income earner in your household, or work in a volatile industry, you may want to increase this up to 1-year.

Additional Reading on Emergency Funds:

HSA

If your health plan qualifies for an HSA (Health Savings Account), this account can serve as a powerful tax-advantaged savings tool. HSAs provide triple-tax advantages: contributions are tax-deductible, the money grows tax-free, and withdrawals for qualified medical expenses are also tax-free. It's effectively the best tax deal around—if you're eligible, don't miss out.

Note: Fidelity offers a fee free HSA that allows you to invest your entire HSA balance. You can roll your HSA into it even if your employer uses another provider.

Additional Readings on HSA’s: (and why I stopped opting for the HDHP)

Max Out Pre-Tax 401k

After securing your match, continue to maximize contributions to your pre-tax 401(k). Reducing your taxable income now can mean significant immediate tax savings, especially beneficial in high-income years. Contribute the maximum allowed annually ($23,500 for 2025) to fully leverage these benefits.

Note: It is important to understand how your 401k match works. I almost lost $5,000 two years in a row from my partner’s Uber 401k by not fully understanding how the True Up worked.

Mega-Backdoor Roth IRA

If your employer allows it, this step is a powerful way to put more money into a tax-advantaged account after you've maxed your standard 401(k). The mega-backdoor Roth allows you to contribute after-tax dollars and immediately convert them to Roth, growing tax-free and eventually withdrawing tax-free. Make sure your employer’s plan supports both after-tax contributions and in-service withdrawals or conversions. If it's not available, just move onto the next step.

Additional Reading:

Note: Some would prioritize the Backdoor Roth IRA first, and that is perfectly fine. I typically point people towards the Mega Backdoor Roth because it is much easier to update your contribution percents than go through the backdoor roth ira process.

Backdoor Roth IRA

After you've leveraged employer-sponsored retirement plans, the next step is the backdoor Roth IRA. This allows higher earners, typically ineligible for direct Roth IRA contributions, to contribute indirectly through a non-deductible traditional IRA contribution and immediate Roth conversion. It's another way to secure tax-free growth and withdrawal in retirement.

Please don’t do this if you currently have a rollover ira or traditional ira! There are steps you will want to complete first.

Additional Reading:

Taxable Investments

This is where you'll put additional savings once you've exhausted other tax-advantaged options. A taxable brokerage account provides flexibility and liquidity, making it ideal for early retirees. There are no penalties for early withdrawal, and it allows you to build wealth that can be accessed whenever you choose.

How to Personalize Your Savings Prioritization

The order above is a solid foundation, but everyone's financial situation is unique. Consider these factors to customize your savings prioritization:

Job Security and Income Predictability: Increase your emergency fund if your income fluctuates or your industry is volatile.

Debt Tolerance: If debt keeps you awake at night, prioritize debt repayment more aggressively.

Family Goals: Adjust funding to your 529 accounts based on how you prioritize education and the expected timeline for these expenses.

Early Retirement Plans: Maximize investments in brokerage accounts for flexibility if planning for early retirement.

Personal Priorities: If early financial independence is your top priority, emphasize taxable investments and Mega-Backdoor Roth contributions.

Mortgages: If you locked in a <4% interest rate, you can probably hold off paying your mortgage down. If you are sitting on a 7%+ interest rate, then I would likely start chipping away at it sooner. Gets much more fuzzy in between those numbers.

Feel free to skip or adjust steps that don't match your personal goals or financial circumstances!

It Doesn’t Need to be Binary

It is very easy to get stuck thinking that saving into different buckets is all or nothing. Reality is rarely all or nothing. It could be perfectly fine to split your prioritizations across multiple categories at once instead of waiting for a prior one to fill up.

“Can you walk me through how your money flows through your accounts?”

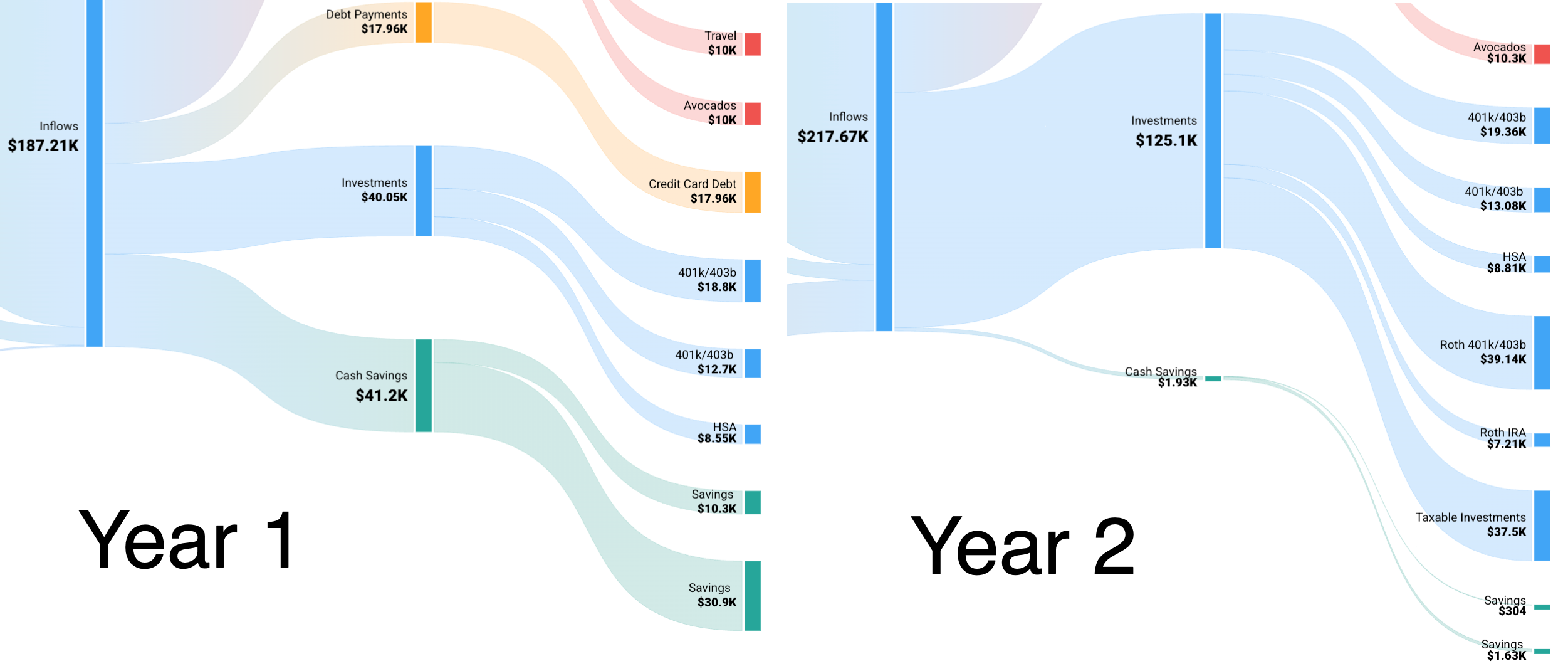

I almost always ask this question during my 1:1 coaching sessions. With more than a decade working on growth, I can’t stop my brain from thinking about things in terms of funnels and waterfalls. If you are like most people, your waterfall is less of a smooth flow… and more of a leaky bucket.

A Well Optimized Flow

In contrast, here is another visual of how this could look over two years following the prioritization flow chart. In the first year you have to build up your 1-month of expenses, pay off your debt, fund your 3 month emergency fund. In the first year it stops before the Mega-Backdoor Roth contributions. Then in year two, it is able to make it through to building up more than $37.5k into the taxable brokerage! At the end of the day it is all about prioritization. You can’t always do everything every year.

I really like to use Projection Lab to create a more granular forward looking waterfalls that help me understand when different buckets will fill up. It also makes it easy to hard code in the specific prioritization, feel free to copy the one I used below:

Remember, personal finance is personal. Understanding the why behind these frameworks will help you align your prioritization with your personal goals.

curious if where would you fit 529s in this waterfall?

If planning to switch jobs midway through year, reversing “finish maxing out 401k” and “mega backdoor Roth” would switch to take advantage of both company matches, correct?